There’s an intrinsic link between risk and return in everything you do and do not. Investing is no different. There is a high correlation between the investment risks and expected returns.

Return is telling only half of the story

The majority of investors tend to judge the success of their investments by the returns they make, but the return tells only half the story. Risk is as important as any other aspect of making an investment decision.

The relationship between risk and return is a fundamental investment concept stating that an increased probability for return is highly correlated with the increase in the level of risk taken. In other words, the higher return the investors are aiming to achieve, the higher risks they should be willing to bear.

The amount of risk an investor is prepared to take is really a matter of personal choice – there’s no “rule of thumb” or “one size fits all” approach. Some investors are very risk-averse, as their only focus is on the avoidance of loss. Others might be ready to take high risks in the anticipation of attractive returns. However, most of the investors fall between those two extremes, ready to take some risks but willing to sacrifice the higher spectrum of the returns to avoid major capital losses.

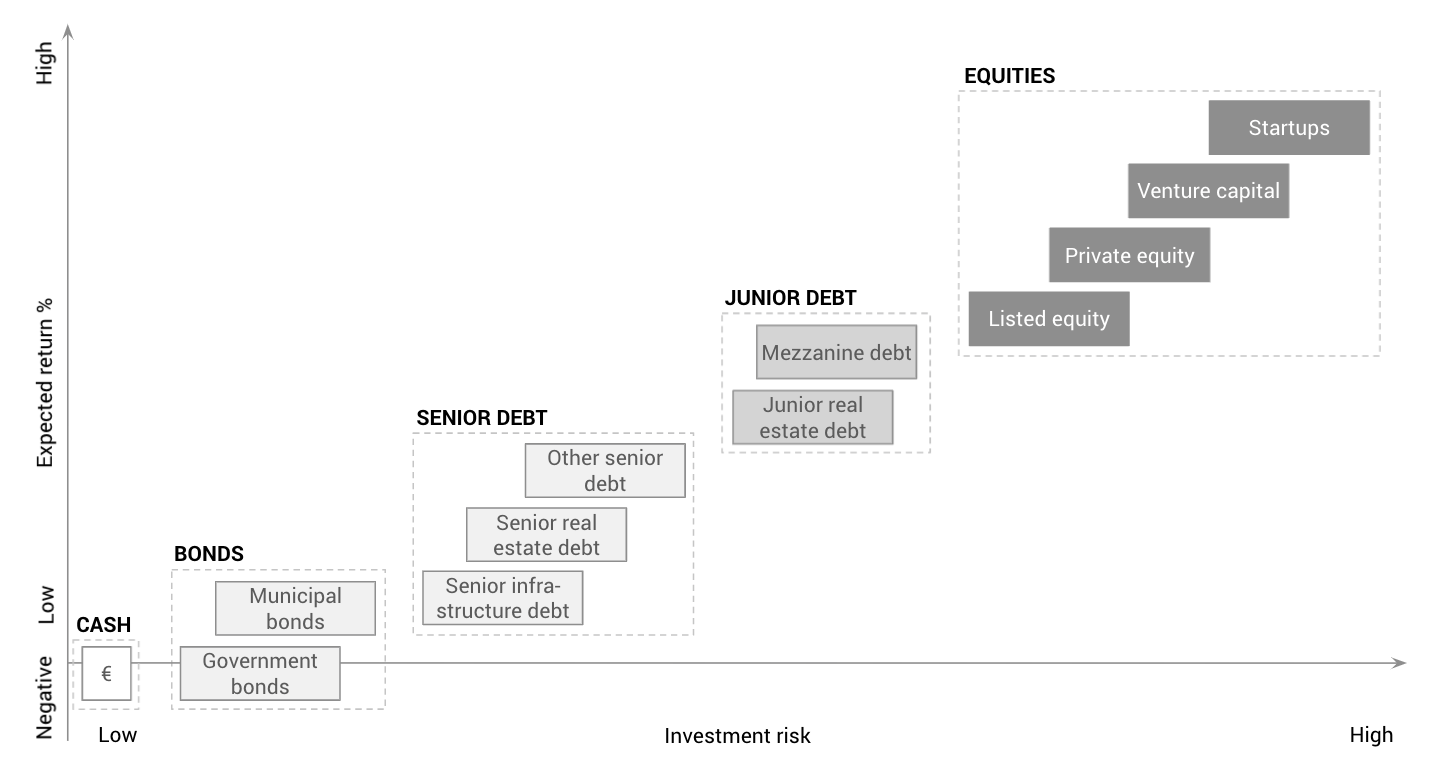

Investment risk and expected return of main investment assets

There are multiple ways to group different asset classes and put them on the risk/return chart. Our favourite way is to split the investable assets into 4 main categories: cash, government bonds, private debt and equities. We have deliberately left out the more exotic investments like unsecured consumer debt and payday loans, cryptocurrencies, etc.

The lowest-risk asset is cash – money in your wallet or in your savings account. Unless you lose your wallet or your savings account balance exceeds the limits established by the government deposit guarantee program, your cash is very safe. However, while your bank might not charge you for the funds in your savings account, inflation is eating the cash’s purchasing power. With Eurozone inflation hitting 10% per annum recently, your money is effectively losing 10% of its value every year.

Government bonds as long as the government retains the right to print more money and this money is generally accepted as the means of payment, government bonds can be considered a very safe investment. The downside of investing in government bonds is their current negative yields – you will have to pay the government to accept your money, and you will receive back less than the original investment amount. Short-term government bonds are currently trading at negative yields, so if you decide to buy some government debt, expect to get less money than initially invested. Do not forget to add the devastating effect of inflation.

Municipal bonds, especially those issued by large municipalities with a broad and healthy tax base, are usually considered safe investments. The smaller the municipality, the higher the risk and the return they have to pay for your loan. Municipalities can go bankrupt (and they have done that as well). Municipal bonds are currently providing a small nominally positive return, but your investment in municipal bonds will still have a negative real return when adjusted with inflation.

Senior debt is a term used to describe a company’s first tier of liabilities, typically secured by a lien against some type of collateral. The investment risk related to senior debt is relatively low. The company is obliged to pay off its senior debt before paying off any other loans, and the senior debt is secured by specific collateral (usually by 1st charge mortgage on a real estate asset). The infrastructure-related senior debt has the lowest yields as it is considered to be the safest type of loan among all senior loans. Senior real estate debt comes right after that and offers slightly better returns than infrastructure debt. The short-term construction loans provided by Crowdestate are an excellent example of senior debt.

Junior debt, also known as subordinated debt or mezzanine debt, refers to bonds or other debts that have been issued with lower priority than senior debt. Junior debt is provided with less valuable, soft collaterals (like commercial pledges, share pledges or personal guarantees) or without any specific collateral at all. The term “junior” means that junior debt is low on the repayment food chain. Junior loans are riskier than senior loans and therefore bear higher interest rates to compensate for the higher risk. Junior or mezzanine debt is an increasingly popular form of borrowing for mid-size and large real estate companies.

Equity is the amount of money that would be left over to the company’s shareholders if all the company’s assets were liquidated and all the company’s debt would be paid off. Investing in equity means that your investment has the lowest priority when returning funds to the shareholders, and thus, such investment is considered the riskiest one. To compensate for the risk of the equity investments, the shareholders are entitled to share the company’s profits. When investing in real estate projects, the return on equity investments will depend on the type and stage of the real estate project.

The equity returns of completed cash flow projects would probably be in the low teens (around 10 per annum, depending on the project’s leverage and terms of senior loans).

The development projects are considered to be riskier due to the uncertainty of the project and the lack of current cash flow, and their expected equity returns would have to be higher to compensate for the additional risks.

Summary

- All of your actions and inactions result in some type of risk;

- There is no “one size fits all” approach when dealing with investment risk and expected return. The final decision is up to yourself;

- The younger you are, the more risk you can bear, and vice versa.

- Not investing or being too conservative will guarantee the loss of purchasing power when inflation eats your savings. Being too aggressive in chasing high returns and taking too much risk can result in sleepless nights and a partial or full loss of your investment.

Revisit our articles on asset allocation (What should you know about asset classes?) and real estate’s share in the investment portfolio (How much should you invest in real estate?).

Proceed to read our next article about investment defaults.

Start or continue your real investing journey with Crowdestate!